Executive Summary

The Affordable Care Act (ACA) expanded access to health insurance for millions of Americans and broadened medical benefits. Under the health reform law, anyone can obtain coverage regardless of age and health status. The law also applied the ACA’s insurance reforms and expanded benefits to individual policies sold outside of government marketplaces.

The Affordable Care Act (ACA) expanded access to health insurance for millions of Americans and broadened medical benefits. Under the health reform law, anyone can obtain coverage regardless of age and health status. The law also applied the ACA’s insurance reforms and expanded benefits to individual policies sold outside of government marketplaces.

Major reforms took effect in 2014, prompting many individuals who lacked coverage, and needed immediate health care services, to enroll for coverage. In addition, many individuals with significant medical conditions had previously been covered through state-based “high-risk” pools, and these people also transitioned into individual coverage. Overall, individual policies before reform offered less generous benefits. The ACA broadened benefits made available to everyone, including, for example, preventive services and screenings, maternity care, disease management, mental health and substance abuse services.

For more than 80 years, Blue Cross and Blue Shield (BCBS) companies have provided secure and stable health coverage to people in communities across the country. As part of this continuing commitment, BCBS companies have participated in the new ACA marketplaces more broadly than any other insurance carrier. As a result, millions of newly enrolled BCBS members are the largest single group of individuals whose health status and use of medical services can be examined for key insights into the medical needs and costs associated with providing care for the new individual market enrollees.

This report is a comprehensive, in-depth study of medical claims among those enrolled in BCBS individual coverage before and after the ACA took effect. In addition, the report also compares the newly enrolled ACA members to those who receive insurance through their employers.

Because the ACA guarantees coverage for pre-existing conditions and broadens benefits available to everyone, individual policies that comply with the law now resemble those offered by employer groups. Thus, comparing the health status, use of medical services and costs of caring for members receiving coverage through the employer market with those covered through ACA-individual policies is important to understanding the dynamics now at work in the health care system.

Comparing the health status and use of medical services among those who enrolled in individual coverage before and after the ACA took effect, as well as those with employer-based health insurance, the study finds that:

Comparing the health status and use of medical services among those who enrolled in individual coverage before and after the ACA took effect, as well as those with employer-based health insurance, the study finds that:

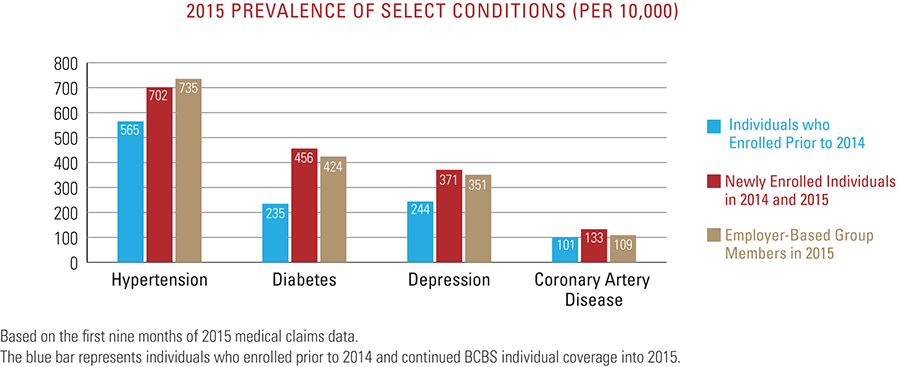

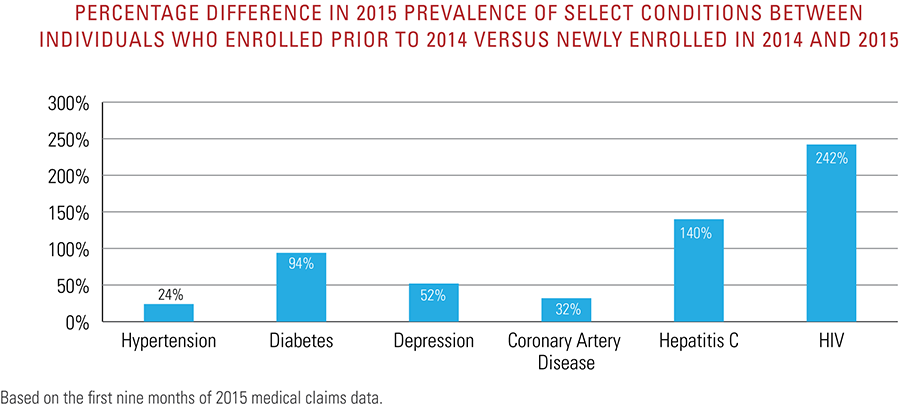

- Members who newly enrolled in BCBS individual health plans in 2014 and 2015 have higher rates of certain diseases such as hypertension, diabetes, depression, coronary artery disease, human immunodeficiency virus (HIV) and Hepatitis C than individuals who already had BCBS individual coverage.

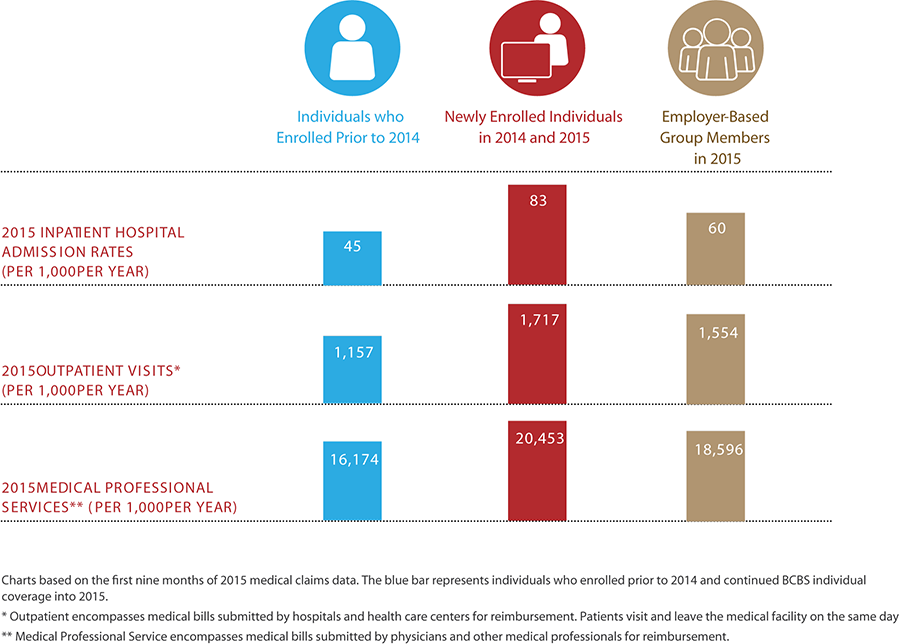

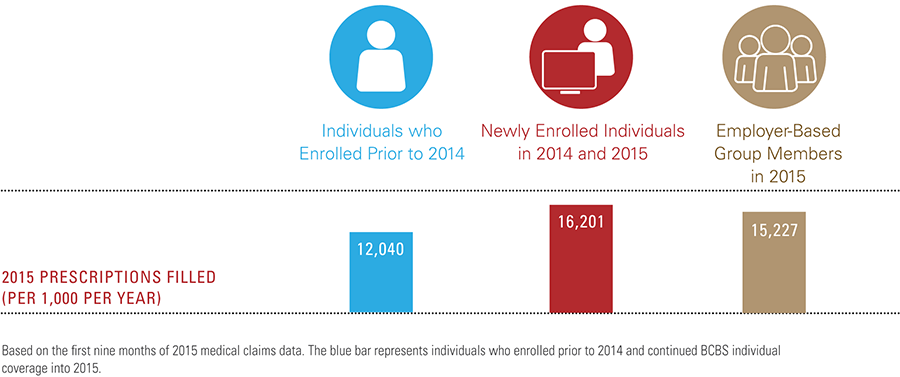

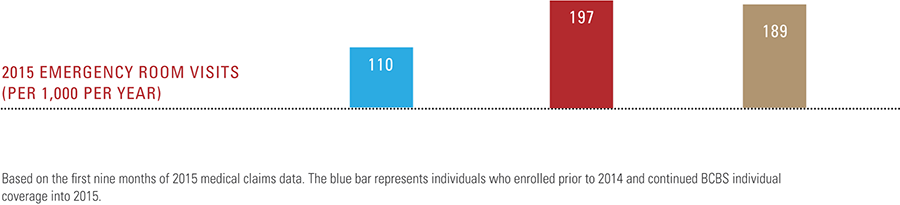

- Consumers who newly enrolled in BCBS individual health plans in 2014 and 2015 received significantly more medical services in their first year of coverage, on average, than those with BCBS individual plans prior to 2014 who maintained BCBS individual health coverage into 2015, as well as those with BCBS employer-based group health coverage.

- The new enrollees used more medical services across all sites of care—including inpatient hospital admissions, outpatient visits, medical professional services, prescriptions filled and emergency room visits.

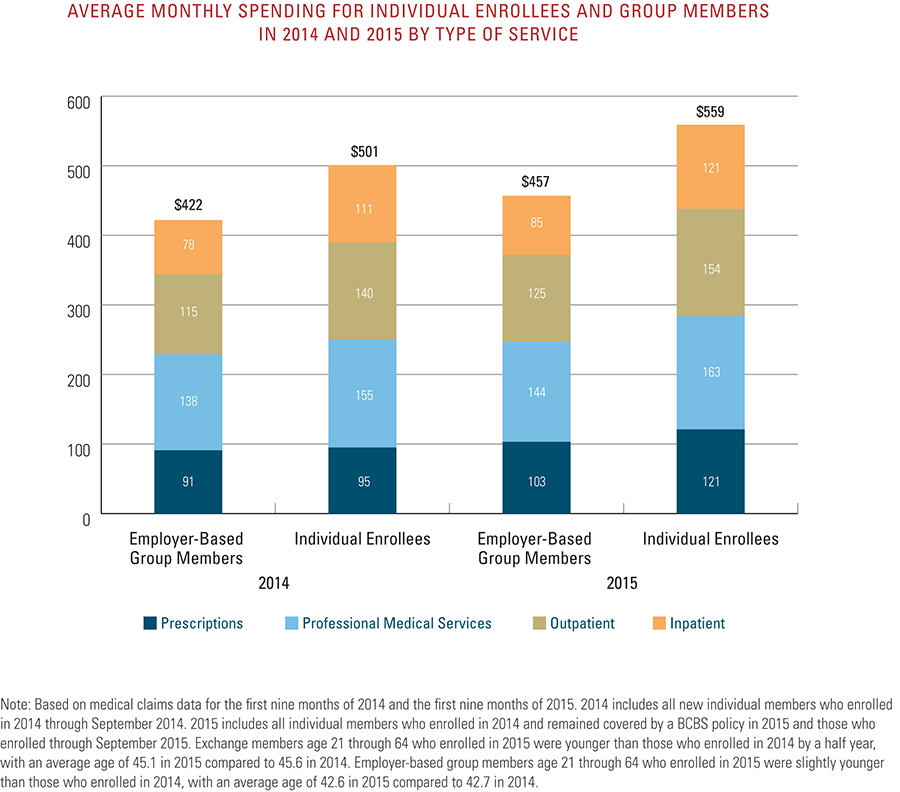

- Medical costs associated with caring for the new individual market enrollees were, on average, 19 percent higher than employer-based group members in 2014 and 22 percent higher in 2015. For example, the average monthly medical spending was $559 for individual enrollees versus $457 for employer-based group members in 2015.

The data underscores the need for health insurers, medical professionals and newly insured consumers to work together to ensure that individuals understand their benefits, and use them to improve their health and well-being. BCBS companies are changing their individual health plan products to enhance care management programs to address the unique needs of this population. In addition, patient-focused care programs that emphasize prevention, wellness and coordinated care—programs that are offered across the country by Blue Cross and Blue Shield companies—can support individuals in getting healthy faster and staying healthy longer.

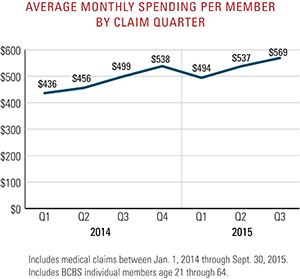

Throughout the first 21 months of healthcare reform, the average medical spending for new BCBS individual members increased steadily, consistent with seasonal patterns and how members typically utilize health benefits throughout the year. More time and data will be needed to understand the long-term health status and costs associated with caring for this new population. In addition, underlying medical-cost inflation and continued demand for medical services will continue to be factors.

Throughout the first 21 months of healthcare reform, the average medical spending for new BCBS individual members increased steadily, consistent with seasonal patterns and how members typically utilize health benefits throughout the year. More time and data will be needed to understand the long-term health status and costs associated with caring for this new population. In addition, underlying medical-cost inflation and continued demand for medical services will continue to be factors.