Executive Summary

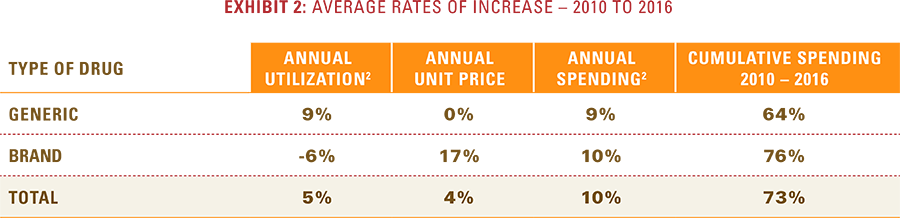

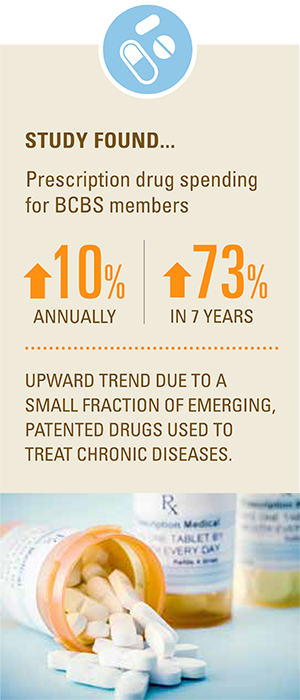

Analysis of a seven-year trend of utilization, price changes and overall spending shows that prescription drug spending has increased 10 percent annually for Blue Cross and Blue Shield (BCBS) members since 2010, an overall rise of 73 percent.1 This upward trend is due to a small fraction of emerging, patented drugs with rapid uptake and large year-over-year price increases that are more than offsetting the continued growth in utilization of lower-cost generic drugs. These higher costs are being incurred by consumers and payers alike; while consumer out-of-pocket costs have risen just three percent annually for prescription drugs in total, they have risen 18 percent annually for patented drugs. Current trends suggest that this rapid rise in drug trend costs is likely to continue in future years.

Specific findings:

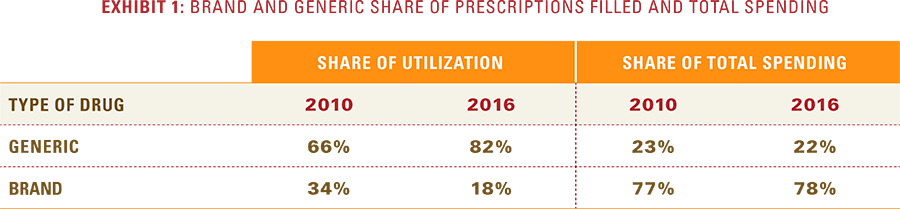

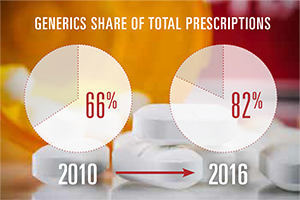

- Over the past seven years, generic drugs increased their share of total prescriptions filled from 66 percent to 82 percent, while brand drugs’ share of total prescriptions declined from 34 percent to 18 percent.

- However, the rising cost of a narrow set of new drugs has resulted in the brand drug market maintaining 78 percent of total drug spending, roughly the same proportion it held in 2010.

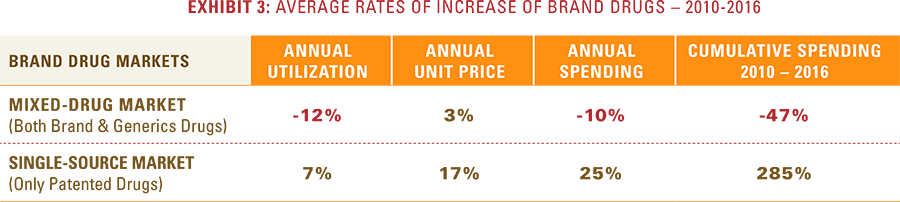

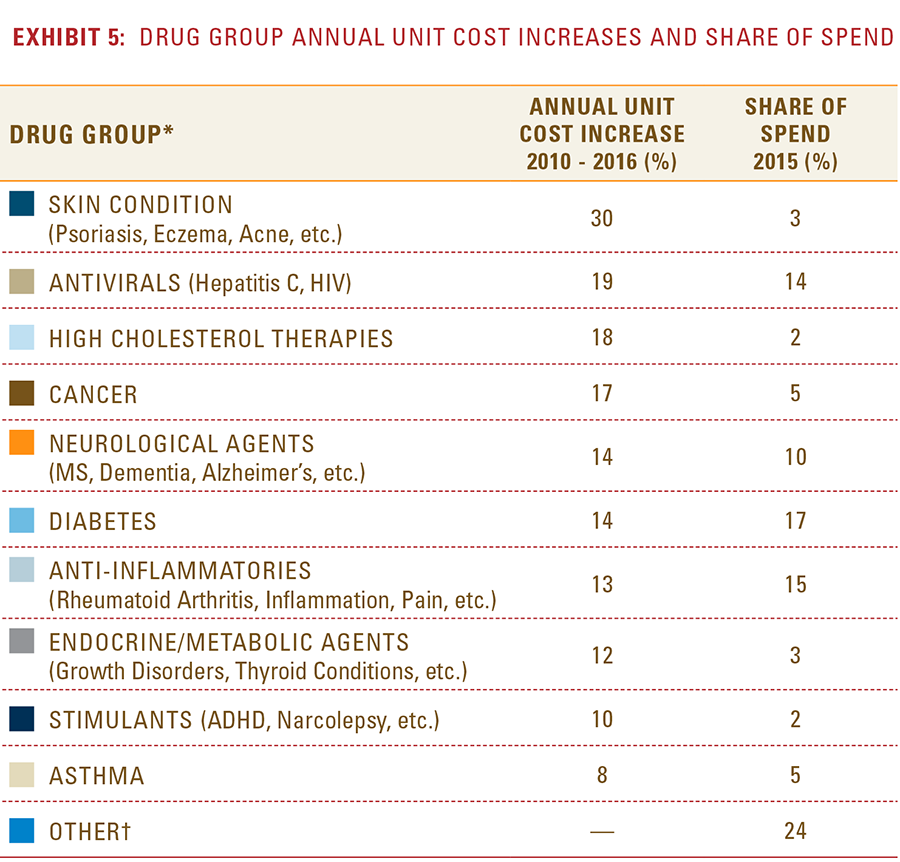

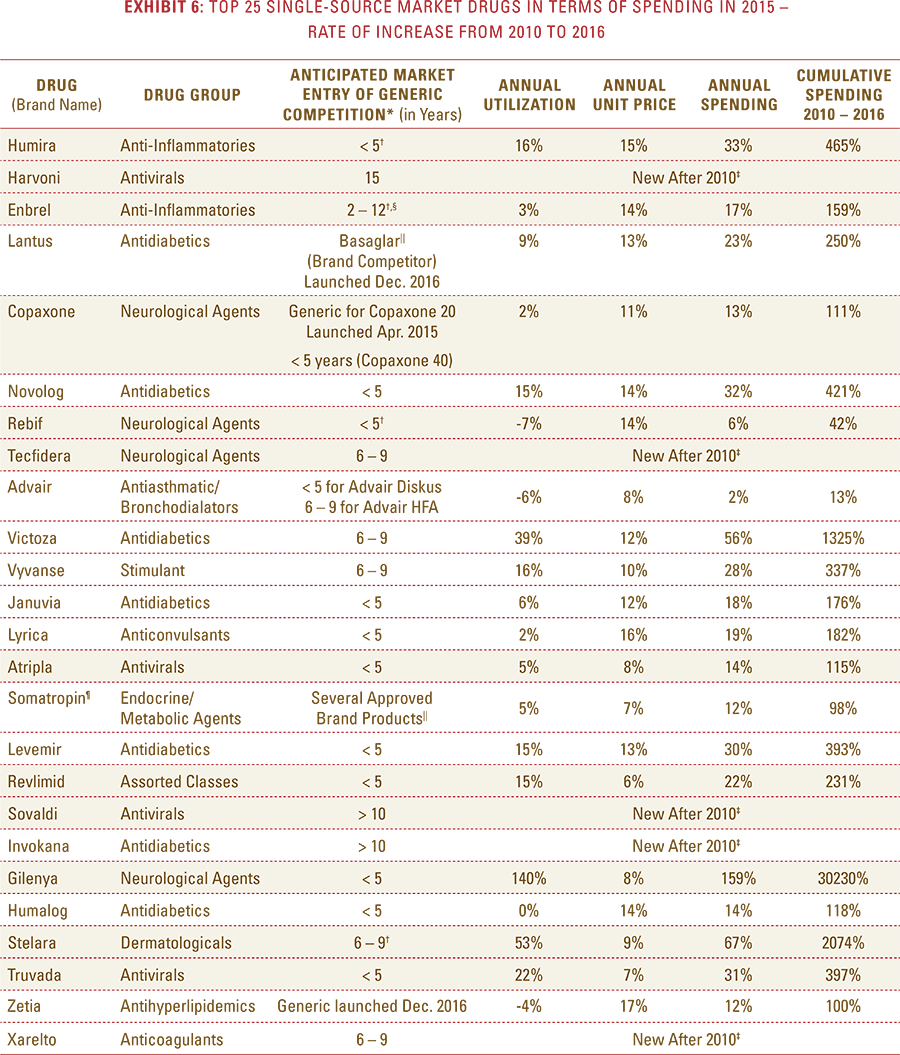

- Specifically, the cost of brand drugs with patent protection and no generic alternatives—commonly referred to as single-source drugs—is rising at an average annual rate of 25 percent (and 285 percent since 2010), more than double the 10 percent average annual rate of spending for all drugs.

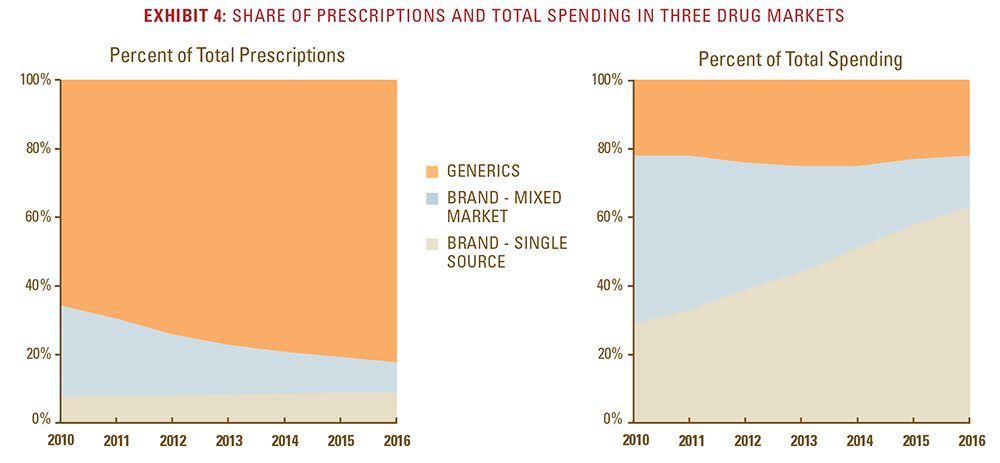

- These patent-protected single-source drugs now make up 63 percent of total drug spending, up from 29 percent of total spending in 2010, despite the fact that they comprise less than 10 percent of total prescriptions filled.

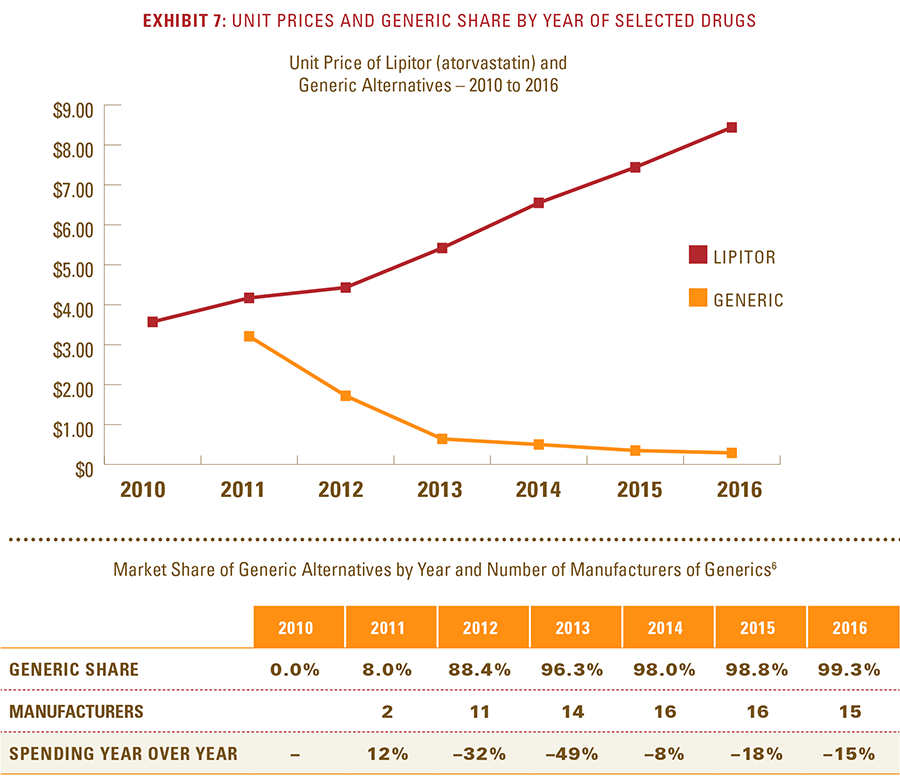

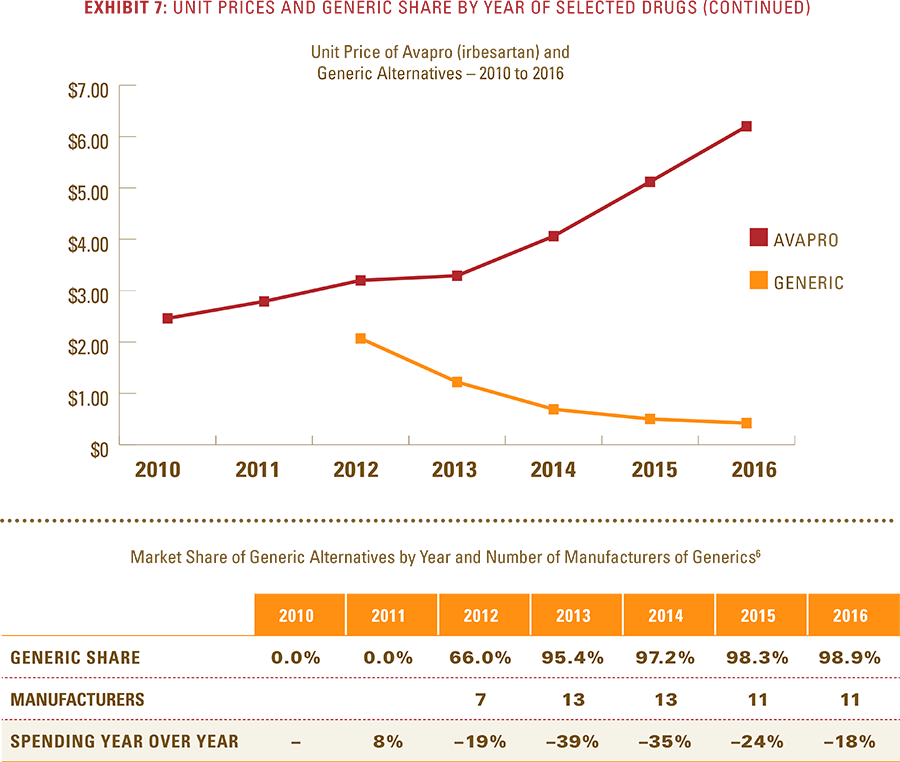

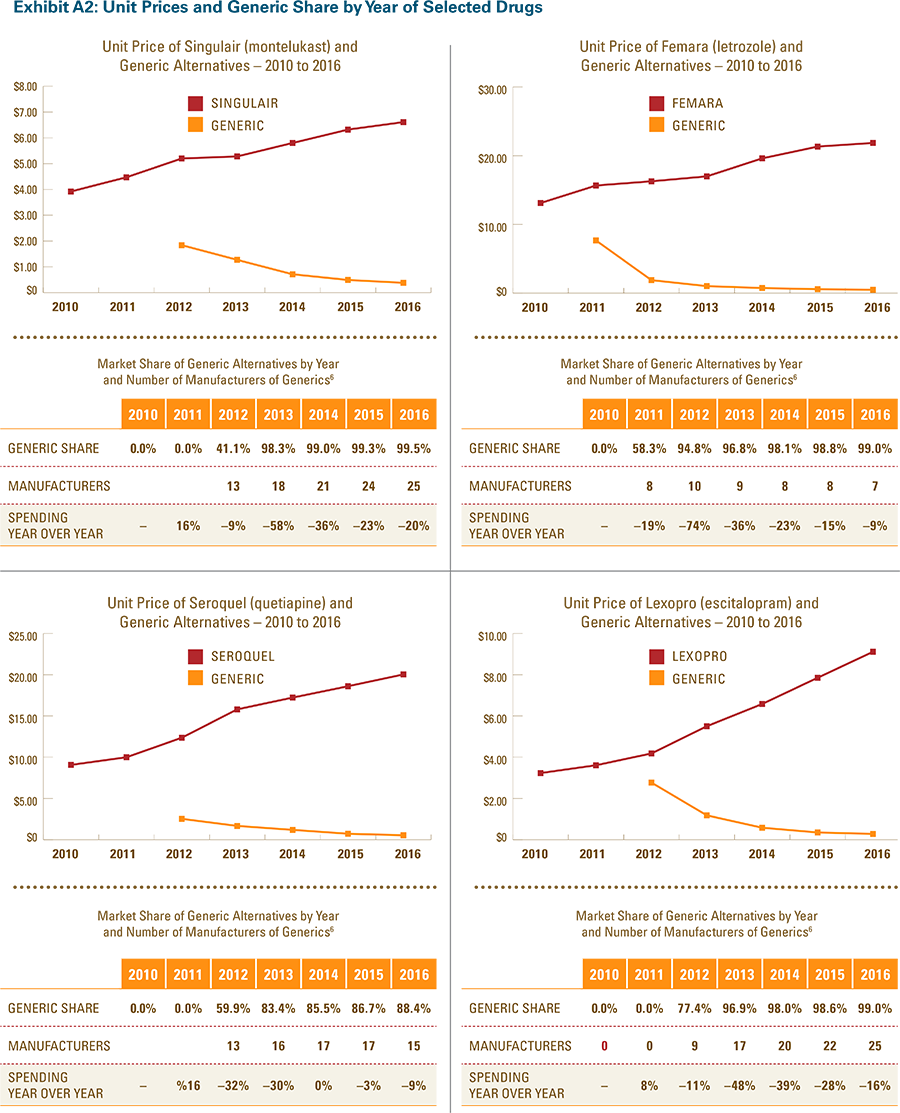

- After a lower-cost generic drug is introduced, the resulting increase in the number of generic manufacturers and the generic share of the market for that drug consistently yields a reduction in total spending within a drug class.

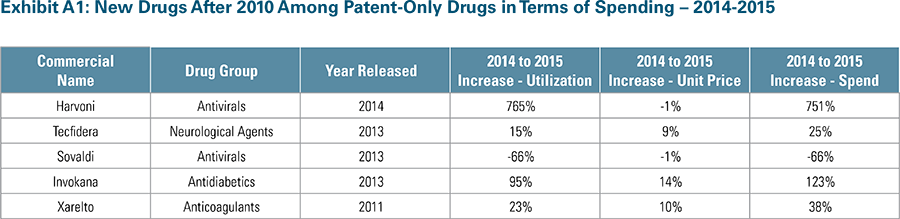

Many of the new brand drugs that are contributing to the rapid rise in drug spending can have life-changing health benefits by treating or managing serious conditions. However, the treatment benefits of these drugs can only be fully attained if they remain affordable over the long term.

1. The cost trends cited in this report are derived from Rx claims data and therefore do not include the impact of drug rebates but does include network discounts. Rebates vary by a number factors (e.g., market segment, insurer, manufacturer, etc). Reporting trend in this way is an industry and actuarial practice for commercial business.

Despite significant increases in the adoption rate for generics, brand drugs still comprise a dominant share of overall drug spending. As Exhibit 1 shows, generics have expanded from 66 percent of all prescriptions in 2010 to nearly 82 percent in 2016. The drop in the share of brand drugs, however, has not lessened their contribution to total prescription drug spending. In fact, that contribution has increased slightly from 77 percent to 78 percent. As generics approach 90 percent of all prescriptions, their rate of increase in share will inevitably begin to slow down. As a result, their ability to offset the rising cost of brand drugs through share growth will diminish.

Despite significant increases in the adoption rate for generics, brand drugs still comprise a dominant share of overall drug spending. As Exhibit 1 shows, generics have expanded from 66 percent of all prescriptions in 2010 to nearly 82 percent in 2016. The drop in the share of brand drugs, however, has not lessened their contribution to total prescription drug spending. In fact, that contribution has increased slightly from 77 percent to 78 percent. As generics approach 90 percent of all prescriptions, their rate of increase in share will inevitably begin to slow down. As a result, their ability to offset the rising cost of brand drugs through share growth will diminish.