Introduction

With the Affordable Care Act (ACA) now in its third open enrollment period, insurance carriers are applying more data – including the actual health care costs of newly-enrolled members – to design offerings that meet the needs of consumers and manage risk for health insurers in this new market. The marketplaces continue to demonstrate that this is a time of transition.

To gain both a national and local picture of how competition and product offerings on the ACA marketplaces have changed in 2016, the Blue Cross Blue Shield Association (BCBSA) compiled and analyzed a county-level database of every individual market health insurance carrier and product sold across the country. Blue Cross and Blue Shield (BCBS) companies participate extensively in the ACA marketplaces, with more members than any other insurance carrier and more extensive geographic coverage.

The analysis includes the findings below:

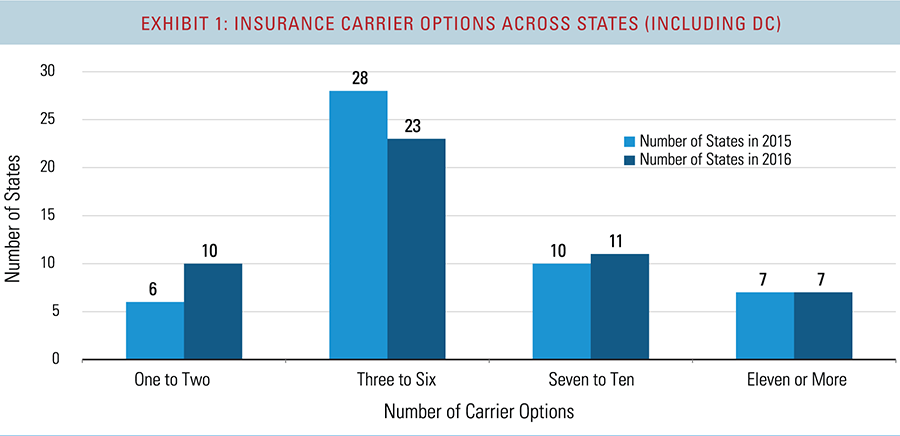

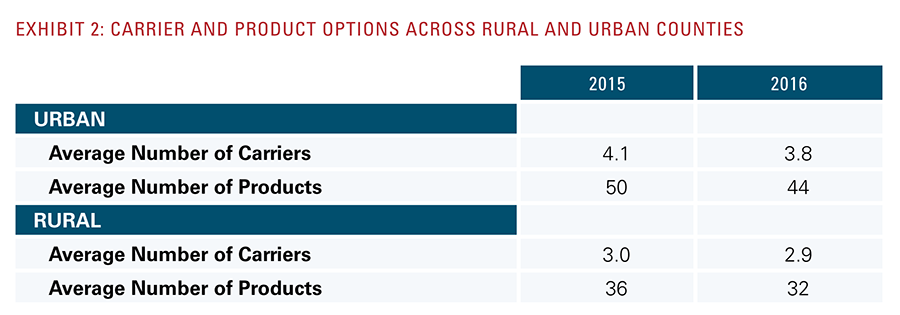

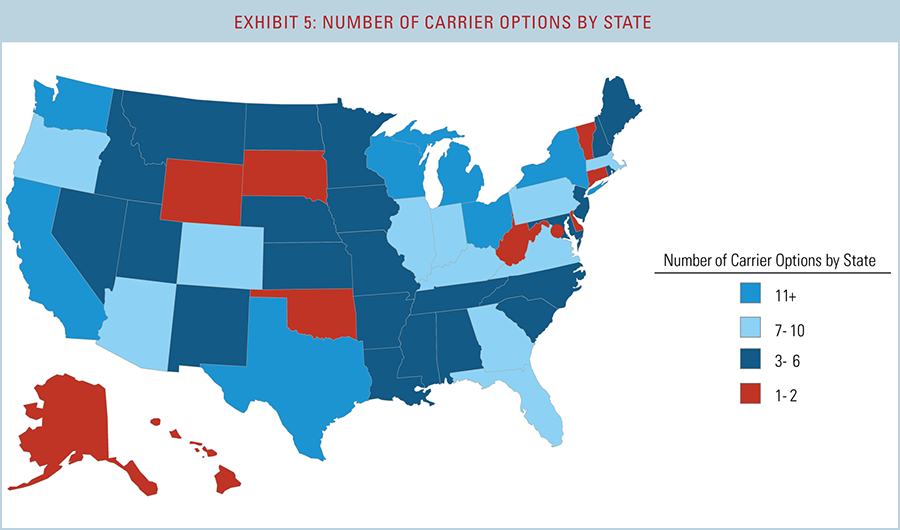

- Continued wide range of insurance carriers and product choices: Although some smaller carriers are no longer offering coverage, choices for consumers are relatively unchanged. On average, consumers in urban markets have 44 product choices in 2016, down slightly from 50 choices in 2015. Rural markets saw a somewhat smaller decline; consumers in those markets have 32 products to choose from, on average – four fewer than they saw in 2015.

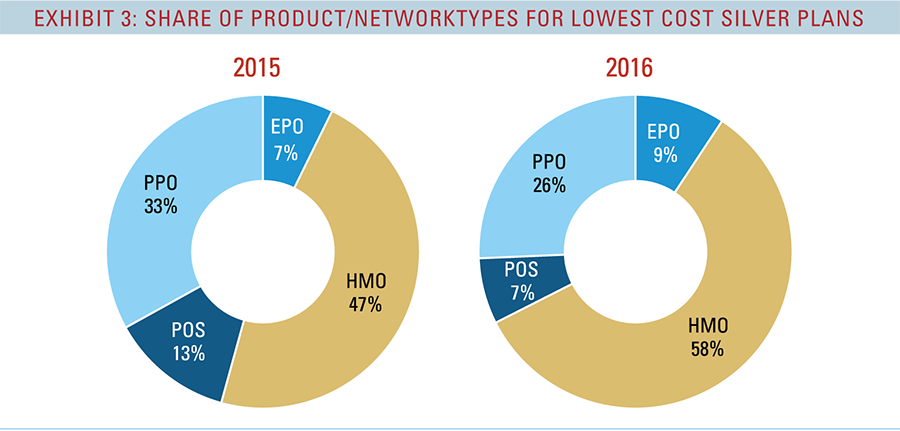

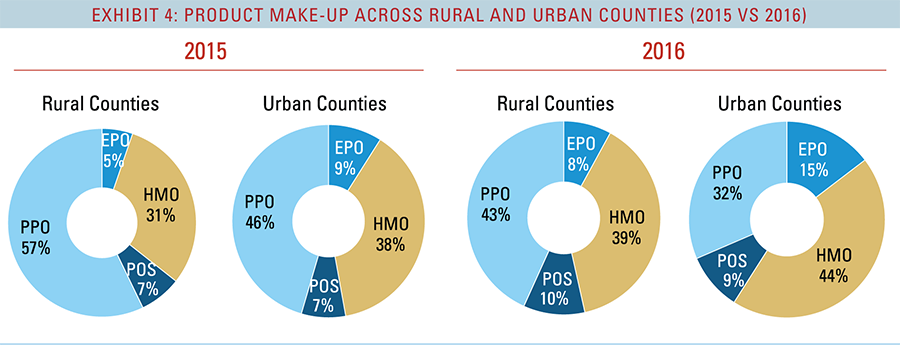

- Carrier offerings are evolving1 : Insurers are offering more product choices with networks and benefits designed to offer options to consumers who are seeking lower out-of-pocket costs. The share of HMO and EPO products offered in the marketplaces increased from 41 percent in 2015 to 52 percent in 2016. In addition, in 2015 the lowest-cost silver product2 in 47 percent of all counties was an HMO product. In 2016, that figure increased to 58 percent. Insurers are also offering varying benefit designs, such as plans that couple a high deductible with two to five primary care physician office visits before the deductible is met.

- Markets are showing less variation in price: With more data and greater experience in this new market, insurers are able to price their products more accurately. In 2014, 53 percent of counties had lowest-cost silver plans priced more than 10 percent lower than the next lowest-cost competitor’s option. In 2016, that number dropped to 38 percent of counties.